“Michelle, last year I lost my job and was unable to keep up with my credit card payments. The credit card accounts have been closed and the accounts are being reported as “charge offs” on my credit reports. I don’t know why, but the accounts are still showing outstanding balances. Since the accounts have been charged off that means that I don’t owe the debt anymore and the balances should be zero, right? What gives?!”

A somewhat common misconception which consumers may have is the idea that if a bill is charged-off then the debt is no longer owed. Unfortunately for the consumer, that is a myth. A charge off does not equal forgiveness of a debt. Charge off is simply a classification or a category that creditors give to debt which they will be writing off as a loss for tax purposes. When a charge off notation appears on a credit report, it does not mean that the consumer no longer owes the balance. The balance may still be very much owed to the creditor or collection agency.

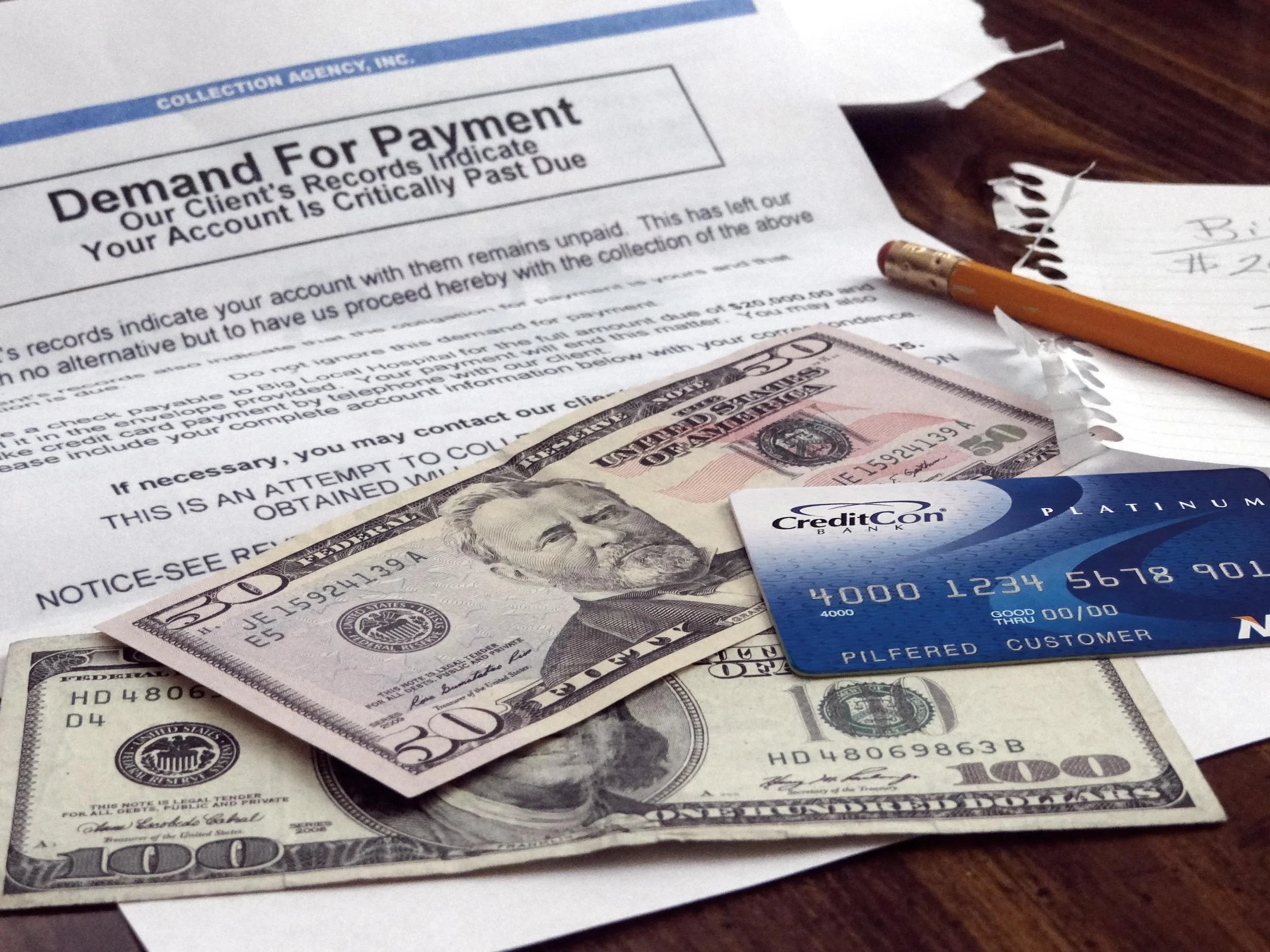

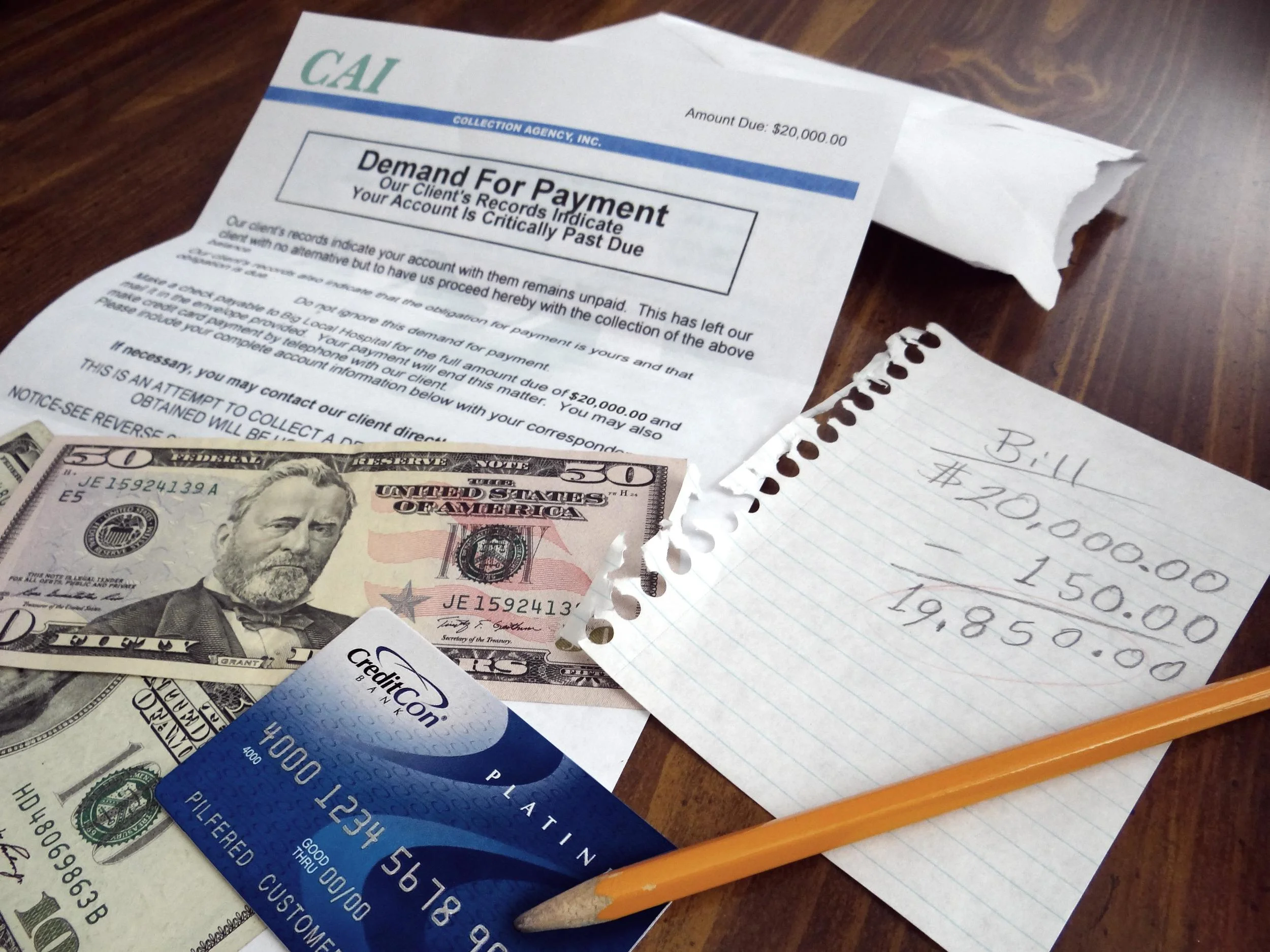

When a debt is charged off by the original creditor (typically once the account has become around 6 months past due), it is often sold or turned over to a collection agency. If you can afford to pay the debt before it is reported to the credit reporting agencies, you should do so. You can save yourself a big headache in the future by paying the account now.

It is also important to be aware of your rights concerning charged off debt. Take a look at the list below to protect yourself from “credit bullies” who are employing abusive or illegal collection tactics.

Know Your Rights

1. FDCPA (Fair Debt Collection Practices Act) -

Collection agencies are not allowed to harass you. They cannot call you excessively, threaten you, or call you at all hours of the night. Collection agencies cannot call your friends and family members in an attempt to embarrass you. There are a lot of other protections afforded to you under the FDCPA. If you have been called or harassed by a collection agency, it might even be in your best interest to speak with an attorney who specializes in FDCPA cases. In fact, feel free to contact us if you would like a referral to a reputable attorney in your area. If you have been harassed then there is a chance your attorney will even represent you on contingency with no upfront funds coming out of your pocket for attorney fees.

2. FCRA (Fair Credit Reporting Act) –

A. Re-aging is illegal.

Derogatory accounts are allowed to remain on your credit reports for 7 years from the date of default (when the original account became 6 months past due). If a collection agency changes the date of default on the original debt in an attempt to manipulate the date when an item is purged from your credit reports, that is known as re-aging and it’s illegal.

B. You have the right to dispute inaccurate, questionable, unverifiable, and outdated accounts.

If you believe that a collection account on your credit reports has been re-aged, you have the right to dispute the account with the credit reporting agencies. You can file disputes on your own, or with the help of a professional like HOPE4USA. You also have the right to dispute any accounts which you believe to be inaccurate or unverifiable.

The best thing that you can do for your credit scores is, of course, to keep all of your payments on time. However, anyone using a little common sense can realize that most people never set out not to pay their bills. It’s not like consumers with credit problems just wake up one morning and say, “I think I’ll stop paying my bills today.” No, most people who get into credit and financial trouble do so due to unfortunate circumstances like job loss, illness, family emergencies, etc. Bad credit happens to good people every single day.

If you have made credit management mistakes in the past, there is good news. Bad credit does not have to last forever. CLICK HERE to download our free HOPE4USA Credit Report Toolkit for some expert advice on how to get started on your road to recovery today!

Michelle Black is an author and leading credit expert with over a decade and a half of experience, a recognized credit expert on talk shows and podcasts nationwide, and a regularly featured speaker at seminars across the country. She is an expert on improving credit scores, budgeting, and identity theft. You can connect with Michelle on the HOPE4USA Facebook page by clicking here.